How your Credit Rating Affects the Cost of Borrowing

Many people ask about their credit and how their credit ratings can affect their ability to finance a vehicle. We've prepared this short article in order to explain the credit rating system and how the banks use credit scores to help make lending decisions.

Your credit score is a measurement of financial reliability; it predicts how likely you are to pay your debts. The impacts of the often-mysterious credit score reach far beyond the credit limit on the plastic card in your wallet. Your credit rating is also a large factor in approval and rates for lending companies and even utility companies, phone companies, or landlords. Credit scores predict the likelihood of on-time, in-full payments over the next 24 months, which is exactly what lenders need to know today.

There are several different models, algorithms, and credit rating bureaus, so you actually have more than just one credit score and they're probably not the same. The algorithms and exact value metrics used by each bureau are kept secret, so knowing how to fix your credit score can feel like an elusive quest. FICO is the biggest name in credit reporting and more than 90% of financial institutions in the US use the FICO score for lending decisions. In Canada there are two major ratings agencies for consumers: Equifax and TransUnion. Even though Canada doesn't use FICO, credit scores in Canada are still often referred to as "FICO" scores.

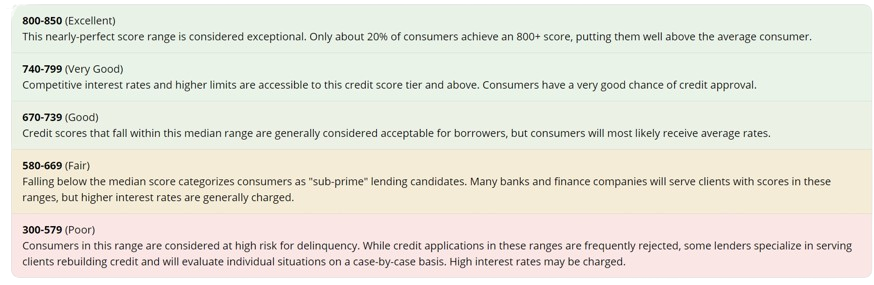

Interpreting your credit score is fairly easy. Credit scores range from 300 to 850. The higher your credit score number, the better! High scores earn the easiest approval processes and the best interest rates. Credit scores essentially fall into five categories:

There are many factors that affect your credit score, including payment history, amounts owed, length of credit history, types of credit, and new credit inquiries or account openings. About 35% of your score is influenced by payment history, including your timeliness of payments.

It's important to note that borrowers with no credit history are given the benefit of the doubt by many lenders. You may be given smaller limits at average interest rates until you build up a credit history.

Credit scores are not at all affected by personal or demographic information. Many consumers are surprised to learn that their income, marital status, and even child support payments have no effect on their credit score. Scoring a big pay raise won't make your credit score budge a bit! Since your credit score is not connected to your income, banks and finance companies will often ask for proof of income in order to fully assess an application.

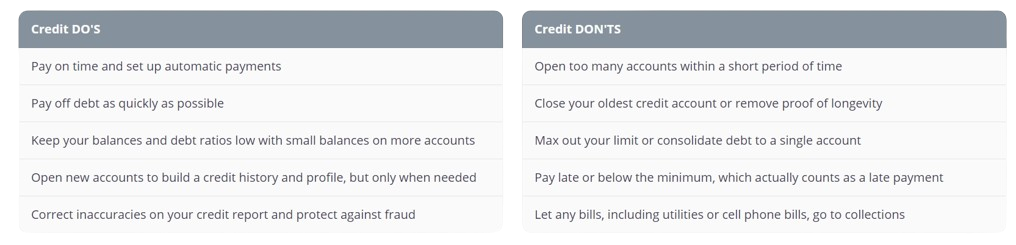

Improving your credit score takes time because it's a 24-month prediction of your financial reliability. Weighty missteps like foreclosures, delinquencies, and bankruptcies can negatively affect your credit for years, even with immediate corrective action. Most of the suggestions and tactics are more preventative than reactive:

Ready to Finance a New or Used Car, Truck, SUV or Van?

Apply now for personalized and professional financing and delivery. We specialize in vehicle financing for residents throughout Canada.